Contents

List of Abbreviations

CBA: Cost Benefit Analysis

CNCA: Corporate Natural Capital Accounting

DCWW: Dŵr Cymru Welsh Water

NC: Natural Capital

NCA: Natural Capital Accounting

NCC: Natural Capital Committee

NRW: Natural Resources Wales

ONS: Office for National Statistics

SSSI: Site of Special Scientific Interest

EXECUTIVE SUMMARY

Key Messages:

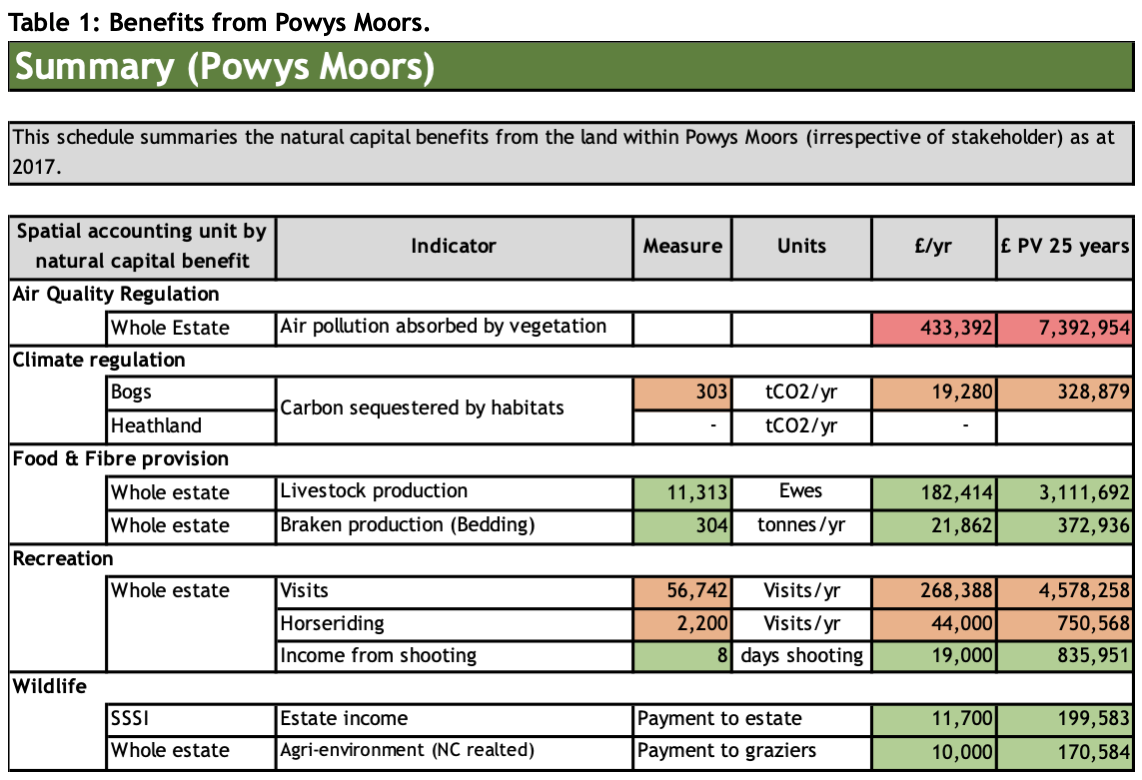

- The natural capital account for the Powys Moors captures over £1m of annual value across 5 benefits.

- The account broadly illustrates the relative values of different benefits, and informs potential synergies and trade-offs between them.

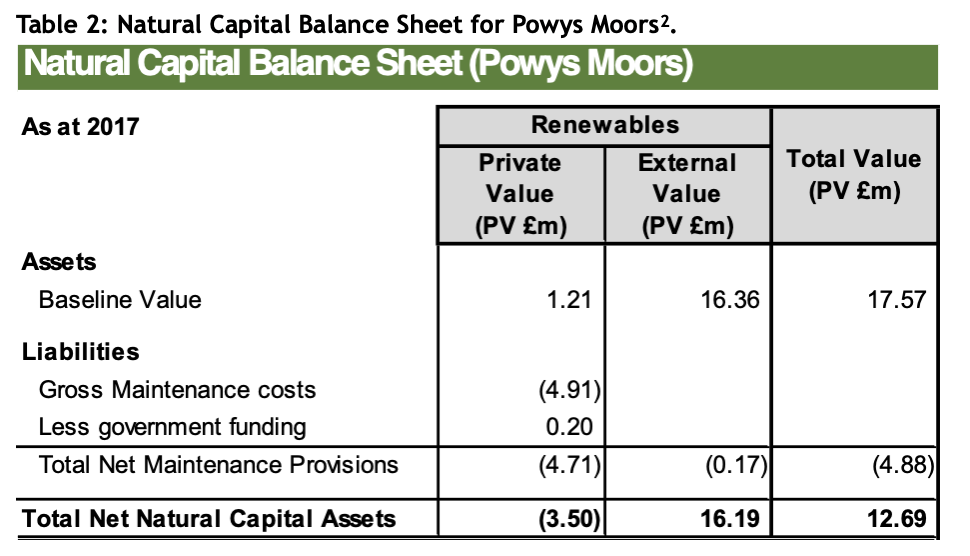

- The balance sheet shows that benefits providing revenues are less than the ongoing management costs (giving a net liability of £3.5m), but wider benefits make the Moors a net asset to society worth £12.7m (both figures assessed over 25 years).

- There are several uncertainties in the data available, which mean some of the values in the account are indicative, and some key values, such as regulation of water flows, are omitted from the physical and monetary parts of the account.

- Further work to understand benefits such as soil carbon storage, air quality regulation would improve the accuracy of the account.

The term ‘Natural Capital’ refers to the “stock of renewable and non-renewable natural resources (e.g. plants, animals, air, water, soils, minerals) that combine to yield a flow of benefits to people.” (Source: Natural Capital Protocol (2016). The Natural Capital Committee’s definition captures the same concepts, in slightly different terms.) It is a relatively new term, but its use in approaches to environmental appraisal and accounting is growing rapidly.

The ‘natural capital approach’ entails defining environmental resources as stocks of capital assets that provide flows of benefits (i.e. ecosystem services); understanding the impacts and dependencies of economic activities on these assets and predicting the future stocks and flows to identify risks and opportunities. The approach is being rapidly picked up by policy makers, businesses and investors across different environmental media and economic sectors.

This natural capital account for the upland common land that is included within the Powys Moorland Partnership is based on an asset register which shows they hold a significant area of heather moorland with extensive wildlife designations and an estimated soil stock of 557,000 tonnes of carbon.

The benefits provided by the Moors are summarised in Table 1. Potentially significant ecosystem services relating to water flow regulation and landscape aesthetic value have not been quantified in this account. For several services values, the estimates have high or very high uncertainty. For recreation and air quality regulation, improved national data sources are expected to be published this year which will give significantly better physical measurement and monetary valuations of these services.

Management costs are obtained from the annual budgets of the landowners and the graziers. The landowners invest private money alongside money from the Sustainable Management Scheme. Both pools of money are centralised within Ireland Moor Conservation Limited, a company that manages all of the Powys moors. This is a 3 year scheme aiming to boost the management of these moorlands. The graziers’ income is entirely separate from the landowners and is managed via Grazing Associations that were formed in the early 2000s as part of the creation of Glastir Commons agri-environment scheme. These associations receive payments from Glastir (as they are set on an income forgone basis) and these payments vary in scale depending upon whether that common is in Glastir Entry or Glastir Advanced. The Advanced scheme is the equivalent of England’s Higher Level Stewardship and receives greater payments in return for greater environmental commitments. In this case, that essentially means reduced stocking and some annual money to helicopter spray the bracken to create more grazing on the moorland fringe.

The annual costs and benefit values are converted to present values using a 3.5% discount rate, as recommended by the HM Treasury Green Book, over 25 years. This results in the balance sheet shown in Table 2. The balance sheet shows a net private cost of running the estate. However, taking into account external values, the balance sheet shows a substantial asset value to society.

The following colour ratings are used on the data in Table 1. Low uncertainty reflects confidence in the evidence that can supported decisions. Very high uncertainty reflects confidence of results to within an order of magnitude only.

(Present Values (PV) calculated at 3.5% discount rate over 25 years.)

(Present Values (PV) calculated at 3.5% discount rate over 25 years.)

1. Introduction

1.1 Aims

This study develops the first natural capital account for the Powys Moors managed by Ireland Moor Conservation Limited. The aim of the account is to demonstrate the current value of the Powys Moors, and provide a baseline to assess the additional value that could be created as a result of the new management agreements under the Nature Fund. To achieve this aim, the ‘corporate natural capital account’ (CNCA) framework is used to assess the benefits provided by the Moors, and the costs of maintaining them.

This has enabled a partial natural capital account to be developed. There is potential to expand the content of the account as new information, from primary research and secondary sources, becomes available. It also provides a baseline for monitoring and evaluation of the management of the Moors, including the actions taken to restore shooting and biodiversity interests under the Nature Fund.

1.2 Natural Capital Approach

Natural capital refers to the stock of natural assets (e.g. habitats consisting of soils, species, freshwater, atmosphere, minerals etc) upon which our economies and societies depend. Like other forms of capital, natural capital produces value for people; in the case of natural capital, this takes the form of environmental ‘goods’ (e.g. timber, fish stocks, minerals) and ‘services’ (e.g. climate, air and water quality regulation). These relationships are shown in Figure 1.1.

Also like other capitals, natural capital can depreciate if it is managed unsustainably or exploited for non-renewable resources. However, with appropriate management, it can also provide renewable benefits that are maintained over time.

Natural assets are the components of the stock of natural capital. These assets can be renewable (such as soils, clean water or wildlife) or non-renewable (e.g. minerals, and fossil fuels which are out of scope for this study). They are defined and measured by a combination of their:

- Extent (i.e. spatial area);

- Condition (e.g. in terms of habitat status or ability to produce benefits); and,

- Spatial configuration (e.g. fragmentation, proximity to beneficiaries) and the way in which different assets function together to produce benefits to people.

Goods and Services. Natural capital assets provide both ecosystem goods/services, and non-biological goods/services (e.g. minerals). Provision of ecosystem services depends upon the extent to which natural capital assets function and operate (i.e. their health) as well as on human activities and the proximity of beneficiary populations.

Economic benefits. Goods and services produce benefits for people, often by combining with inputs from other (e.g. built, human and financial) forms of capital, such as veterinary services for the farming of livestock. Some ecosystem services have an obvious relationship to socio-economic benefits, such as the ecosystem sevice of the provision of game birds for the benefits of food and the recreational activity of shooting. Others are more complex, for example waste breakdown supports the health of ecosystems that underpin the provision of livestock, and the maintenance of clean waters for water supply.

The term ‘economic’ is used in its broader meaning incorporating both financial (market) and wellbeing (non-market) benefits. The relationship between ecosystem services and economic benefits varies, and sometimes they can be analysed in a combined manner. However, their distinction can be useful, firstly because some services help provide more than one benefit (e.g. livestock support food provision, but can also contribute to a landscape that supports recreation benefits). Secondly, it helps distinguish physical mesurement of ecosystem services flows from monetary valuations of benefits to people.

1.3 Structure of the Report

In addition to this introduction, the report contains the following sections:

- Section 2 details the scope and methodology used to create the accounts

- Section 3 describes quantification and valuation of assets, physical benefit flows, and monetray benefit flows.

- Section 4 draws conclusions

Details of the calculations and assumptions are contained in a spreadsheet that accompanies this report.

2. Methodology & Scope

2.1 Method

The structure of the Powys Moors natural capital account is based on the ‘corporate natural capital account’ (CNCA) framework. This comprises four supporting schedules populated with data from financial accounts and environmental management information:

- Asset register: The asset register captures evidence on the extent, condition, and spatial configuration of natural capital across the estate;

- Physical flow account: This account records the flows of outputs that the natural capital assets produce, covering both market and non-market goods and services;

- Monetary account: This records the ‘private’ values in terms of income (from market goods and services), and the ‘external’ value to wider society (from non-market goods and services), derived from the estate; and

- Maintenance cost account: This account details the activities and expenditures associated with the management of the estate.

The supporting schedules input to a Natural capital balance sheet. This reports the value that natural capital has capacity to generate over time (the asset value) and the costs of its management over time (liabilities). If the account is repeated over time, this can also provide a statement of changes in natural assets, reporting movements in asset values and liabilities.

2.2 Scope

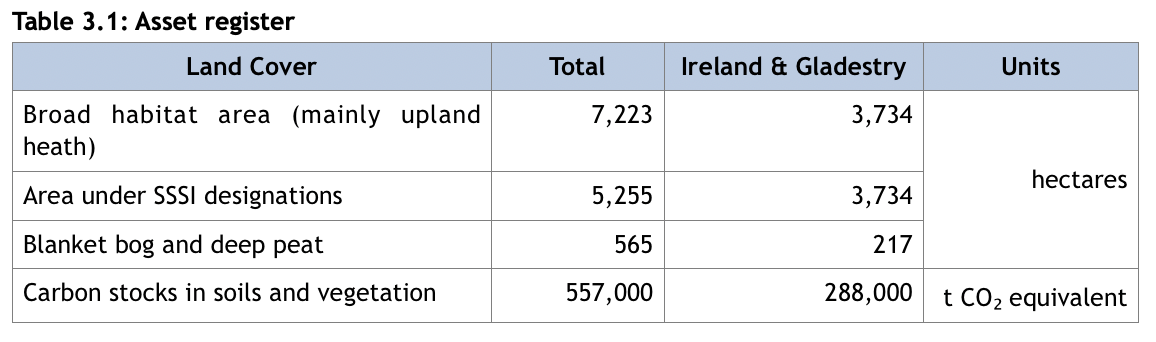

The account has been prepared for the following Powys Moors: Ireland Moor, Gladestry, Beacon Hill, Llanbister and Llananthony. They have a total spatial area of 7,223 ha. Within this area, two moors have more data available: Ireland Moor and Gladestry, with a combined area of 3,743 ha. Therefore, most of the detail in the account relates to Ireland Moor and Gladestry only.

The accounting process considered all those asset types and benefits potentially relevant to the moors. However, the level of analysis of some benefits is restricted by data availability. Where this is the case, an outline of further work required is described for each benefit in Section 3.

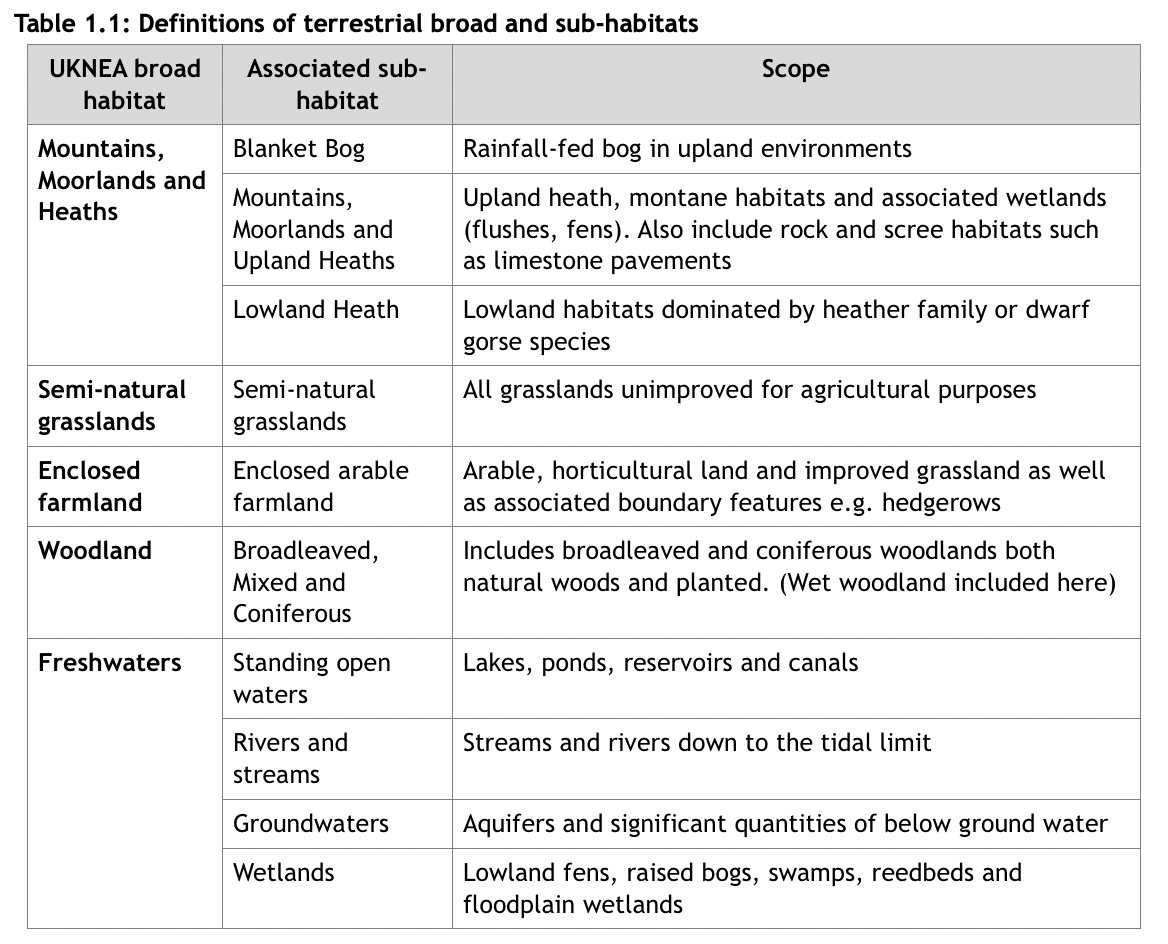

There are eight broad habitat types defined from the UK National Ecosystem Assessment (2011) ‘broad’ habitat definitions and used by the Natural Capital Committee and in UK national natural capital accounting work by ONS. Among these, the ‘coastal margins’, ‘marine’, and ‘urban’ asset types clearly are not present in the Powys Moors, so are not considered further. Table 1.1 shows the other five terrestrial land cover type definitions used within the account to classify natural capital assets.

Timescales are an important dimension of a natural capital account. The Powys Moors account is constructed for 2017 and costs and benefits are discounted over a period of 25 years. This timescale was chosen to balance between a short-term business perspective, and the need to capture costs and benefits from environmental management in the longer-term.

A specific focus of the Powys Moors project is the restoration of peatland and heathland environments. Therefore relevant sub-habitats are used in the account. Peatland is defined as the presence of deep peat soils over 40cm in England and 50cm in Scotland (Crichton Carbon Centre et al (2015) Developing Peatland Carbon Metrics and Financial Modelling to Inform the Pilot Phase UK Peatland Code), and includes raised bogs and fens classified in Table 1.1 as “Open water, wetlands, floodplains”, as well as blanket bogs classified under “Mountains, moorlands and heaths”. The natural capital assets are measured through their spatial extent and condition. The latter brings in information on the quality of habitats (e.g. as indicated by designations) and stocks of stored carbon.

The national natural capital accounts also define a series of benefits from natural capital, on which economic valuations are based. Of these, energy production and minerals are currently irrelevant to the Powys Moors, so are not considered further. The remaining benefits that are considered for inclusion in the account are:

- Aesthetics

- Clean Air

- Clean Water

- Carbon Sequestered

- Food

- Fibre

- Hazard Protection

- Recreation

- Biodiversity

3. Assessment of natural capital assets and benefits

This Section describes the main components of the account. More detail on assumptions is provided in the accompanying spreadsheets.

3.1 Natural Capital Asset Register

The Powys Moors cover 7,223 hectares, all of which is classified as mountain, moor and heath. Around 10% of the land is thought to be blanket bog/deep peat, but the majority of the area (approximately 90%) is heathland. Therefore, the habitat apart from the blanket bog is assumed to be dry upland heath. While the heathland habitats are classified as ‘dry’ they contain extensive areas of shallow peat soils, and some more heavily waterlogged areas with deeper peat. Therefore, these habitat classifications are a simplication for the purposes of the account. As shown in the asset register summarised in Table 3.1, a large area of the land is designated as SSSI.

The vast majority (over 95%) of the estimated stored carbon is in the soil. However, the estimate of carbon storage has significant uncertainty, due to uncertainties over soil depth across the large areas of land considered. In particular, estimates of deep peat can vary with data set used, and can have a significant impact on the estimate of carbon stored.

The designated habitats at Ireland Moor and Gladestry are currently the subject of management to improve their conservation status. The moors contain extensive areas with open public access, public footpaths, and access points. Together these are important parts of the recreational asset the moors provide.

As stated above, 90% of the area is upland heath, part of the ‘mountain, moor and heath’ broad habitat. However, there are also small areas of other habitats, including:

- Freshwater: there are pools, such as on Ireland Moor, with permanent open water.

- Bracken: mainly on the slopes of the moors.

- Grassland: there are fragments of grass habitats amongst the heathland.

- Trees: there are isolated trees across the moorland, but no blocks of trees that would constitute woodland habitat.

While not extensive areas of habitat, these are an important source of habitat variation for both the wildlife and recreational interests at the site. They are retained with the account matrix (see Figure 3.1) to accommodate information on them that could become available in the future.

3.2 Natural Capital Benefits

The following benefits are considered for the account but not quantified:

3.2.1. Aesthetics

The Powys Moors are part of a distinctive rural landscape. Appraisal of landscape value uses qualitative methods (e.g. Natural England, 2014) and there is no monetary valuation evidence available for the overall value of landscape or a marginal change in the aesthetic quality of the landscape that might result from moorland management. This service is therefore not separately quantified or valued in the account. The value of the landscape is however partly reflected in the values for recreation, as it is one of the factors that can motivate recreational visits.

3.2.2. Clean Water and Hazard Protection

Regulation of the quality and quantity of water supplies, and of runoff during flood events, are a difficult set of services to quantify and value. This is because it is very context specific, relating to surrounding landscape (habitat and slope), catchment conditions and impacts on water supplies/ properties at risk of flooding.

The moors are potentially important for water supply, being significant areas of land at the tops of their catchments. A first step in any analysis would be to understand what percentage of the catchment area they make up, both within the entire catchments, and the sub-catchment upstream of the first major assets affected (i.e. water abstraction points or assets vulnerable to flooding).

However, it should be noted that land surrounding the moors has steeper slopes than the moors themselves, and often less vegetation (being predominantly heavily grazed grasslands). These areas may therefore be the primary source of runoff problems causing water quality and flood risks in the catchments. It is in Dŵr Cymru Welsh Water’s (DCWW) interests to understand the condition of catchments and support habitat management that results in a healthy hydrology and avoids water treatment and flooding costs. It is also noteworthy that some parts of the moors drain into catchments in Severn Trent Water’s service area, and so there may be a case for partnership working between the water companies.

This service is not included in the account, but can be examined through further hydrological modelling, ideally in partnership with Welsh Water and/or Natural Resources Wales.

The following benefits are quantified and/or valued in the account:

3.2.3. Clean Air

Detailed modelling of vegetation’s role in mitigating air quality damage has recently be undertaken in the UK to include national pollution removal in ecosystem accounts (Jones et al, 2017). A simple breakdown of the figures can identify the average per-ha values for woodland and non-woodland habitats in urban and non-urban areas. They show a very large range, illustrating the variability in the value of this ecosystem service, primarily because the most significant damages caused by air pollution are to human health, and are therefore highly dependent on how air pollution reaches the people. However, these figures are the result of comparing different versions of the modelling conducted by Jones et al (2017) so are only indicative of the order of magnitude of likely values. Further modelling for the purposes of identifying representative values for different land types and locations are ongoing, and expected to be available during 2018.

The value of this service is estimated from this national data, giving a value of £235/ha for this service in non-woodland habitats in the UK. This gives a whole estate value of £433k/yr, including a value for Ireland Moor and Gladestry of £225k/yr. It should be noted that the Powys Moors might be expected to have a lower than average value for this service, due to their remote rural location resulting in lower air pollution load and fewer people exposed to that pollution. There is a risk that the value of this service is significantly over-estimated, and it has a very high level of uncertainty.

3.2.4. Carbon Sequestered

As described in the asset register, there is substantial store of carbon in the soils on the Powys Moors. However, this service relates to the flux of carbon between these habitats and the atmosphere each year.

The physical measures of carbon storage and sequestration were assessed separately for heathland and blanket bog. The estimates are based on land area and the following assumptions and sources:

- Carbon storage and sequestration was evaluated based on the average carbon equivalent stored per hectare of land type as supplied in the Lake District National Park guide: Managing land for carbon booklet (See page 18 of http://www.lakedistrict.gov.uk/…), Smyth et al (2015) and the Natural England Research Report NERR043: Carbon Storage by Habitat (Natural England (2012), Carbon Storage by Habitat: Review of the evidence of the impacts of management decisions and condition of carbon stores and sources, at:

http://sciencesearch.defra.gov.uk/…). - Annual sequestration was assessed and 4.11tCO2e/ha/year for raised blanket bog.

- There is net sequestration of carbon dioxide, but emissions of methane and dissolved organic carbon (Smyth, 2015). Depending on the condition of the vegetation and peat soils, there are likely to be some areas of dry heath in the Powys Moors that are net emitters, and other areas that are net sequesterers of carbon. Overall the estimated rate of carbon dioxide-equivalent sequestration on the dry heath is assumed to be close to zero.

- Net Sequestration is valued at the non-traded price of carbon provided by the Department of Business Energy and Industrial Strategy (BEIS, 2017). For 2017 the central non-traded value was £63.66/tCO2 (Not that values increase over time – for an explanation of traded and non-trade carbon values, see Annex 1.).

There are an estimated 557,000 tonnes of carbon stored in the soils of the Powys Moors.

The measurement of carbon fluxes is a complex area of science, and can vary over time as habitats are managed. The exact condition of all heathland within the project scope is not known – if actual condition were less than near-natural then the peatland would be a significant net emitter of carbon. Therefore, this estimate has a high level of uncertainty.

It should be noted that many upland peatland soils in the UK are in poor condition (UKNEA, 2011). Therefore, the major benefit of maintaining healthy peatland habitats is to avoid emitting the substantial stores of carbon they hold. Emissions from actively eroding peatland are an order of magnitude greater than from other conditions classified in Smyth et al (2015).

Net sequestration is estimated for the 74ha blanket bog (areas identified as deep peat through -the use of CEH mapped areas of peat soils for Gladestry/Ireland Moor and extrapolated on the same proportion of area for the other Powys moors). The total carbon sequestration is 303 tonnes/yr, which has a current estimated value of £19k/yr.

The account does not consider the emissions from livestock, which can be a significant source of methane and other greenhouse gases – UK sheep can emit over 15 tonnes of CO2eq per tonne of meat produced (Jones et al 2008). Average global FAO figures are 23.4tCO2e per tonne of sheep protein produced, although Western European figures tend to be slightly lower than the global average.

3.2.5. Food

Estimates of food production were based on an assessment of sheep stocking rates at Ireland Moor. From correspondence up to 3,000 sheep were grazed on the 2,750 ha of Ireland Moor, giving a stocking rate of 1.1 sheep per ha. On Gladestry common, the average stocking rate is c.1200 or 1.1 sheep per ha. On Beacon and Llanbister hills the total number of sheep is around 6,000 (giving an average stocking rate of 2.4/ha. The lower figure of 1.1/ha was used to estimate the stocking ratefor the remaining moor, Llanathony. .

This produced an estimate of 11,300 sheep annually and for the monetary account, a gross margin of £50.43 per sheep was assumed (Aberystwyth University Farm Business Survey, 2013/14 Results, p20. Figure of £48.70, quoted in 2013/14 report was uplifted by CPI factor of 3.6% to bring into 2017 prices.). This value is produced from the livestock system that relies on the both moorland grazing and in-bye rearing. Assuming 50% of the value is derived from moor grazing, results in a monetary estimate of £285k/yr. for all of Powys Moors and £106k/yr. for Gladestry/Ireland Moor combined.This assumption can be justified in the knowledge that none of the Powys Moors have zero winter stocking – though reduced in recent years there are still quite a number of graziers who have sheep on the moors all year round.

It should be noted that the grazing is dependent on adjacent areas for livestock management (e.g. lambing) and on farm payments under the rural development programme. Pillar 1 payments relating to the Moors are not known, as they are individually negotiated for common grazing areas in Wales. The average payment in Wales is £134/ha, but moorland payments are understood to be nearer to £20/ha. The account spreadsheet allows for a Pillar 1 figure per ha to be added to the costs, and this would reduce the net value of food production significantly.

3.2.6. Fibre

This includes production of timber and other materials. Bracken is cut from the moors, but is understood to mainly be used for bedding within livestock production. Cut bracken in the UK is not typically sold off-farm (ADAS, 2011). Costs of production usually consist of on-farm cutting, bailing and transportation.

Approximately 200 ha of moorland slopes are cut for bracken per annum on a rotational basis, yielding an estimated 6 bales, or 1.5 tonnes/ha. The annual output of 300t is assumed to avoid the costs of the same mass of straw, currently priced at £28/bale or around £112/t. Set against this cost saving are the farmer’s costs of cutting, baling and transporting the bracken, assumed to be mainly labour at around £10 per bale. These assumptions give a net cost saving of £18 per bale, or £22k/year.

3.2.7. Recreation

. Detailed modelling of recreational activity through the ORVal tool (University of Exeter, 2016) has recently been extended to Wales (June 2018). This tool has been used to provide estimates on the number of annual visits to Gladestry/Ireland Moor (27,500 visits) and their associated monetary value (£130k). These values have been extrapolated to the other Powys moors on the basis of area, giving estimates of 56,742 visits per year, and a benefit value of £268.4k per year for all moors. These estimates cover basic outdoor recreation, which largely covers walking, dog-walking, nature-watching and orienteering and yield an average value of £4.73 per visit using ORVal assumptions.

Information on the days of specialist recreational activity at both Ireland Moor and Gladestry has provided an indication of the range of recreational activity on the moors and provides a basis for some of these activities to be valued in monetary terms.

The number of horse riders visiting Ireland Moor annually was estimated based on three components:

- 50 days activity and assuming an average of ten riders per day, giving 500 riding visits annually.

- Three different trail hunts using the moors annually, giving approximately 400 rides.

- A local pony trekking business that probably uses the Moors for around 300 rides per year.

This gives an overall estimate of 1,200 rides per year for Ireland Moor. Beacon hill is also very popular for horse riding, and along with Llanbister, it was assumed that around 1,000 rides per year are taken on these moors. These visits are valued at a rate of £20/visit for horse riders based on Sen (2014). This gives an estimated annual value of this recreation of £312k per year. This valuation reflects the enjoyment of the visitors, rather than any market purchase.

There is also grouse shooting on Ireland Moor and Gladestry, generating an estimated annual income of £19k in 2017. It is expected that the number of shooting days will increase and that income will rise steadily to around £60k/year over the next ten years. However, it should be noted that this is a revenue to the estate, and does not measure any welfare benefit to shooters, over and above the price of the activity.

The estimated total current annual value of recreation at Ireland Moor and Gladestry is approximately £64k/yr, but potentially rising to around £105k/year by 2027.

3.2.8. Biodiversity

The extensive nature conservation designations indicate the significant biodiversity value of the Powys Moors to society.

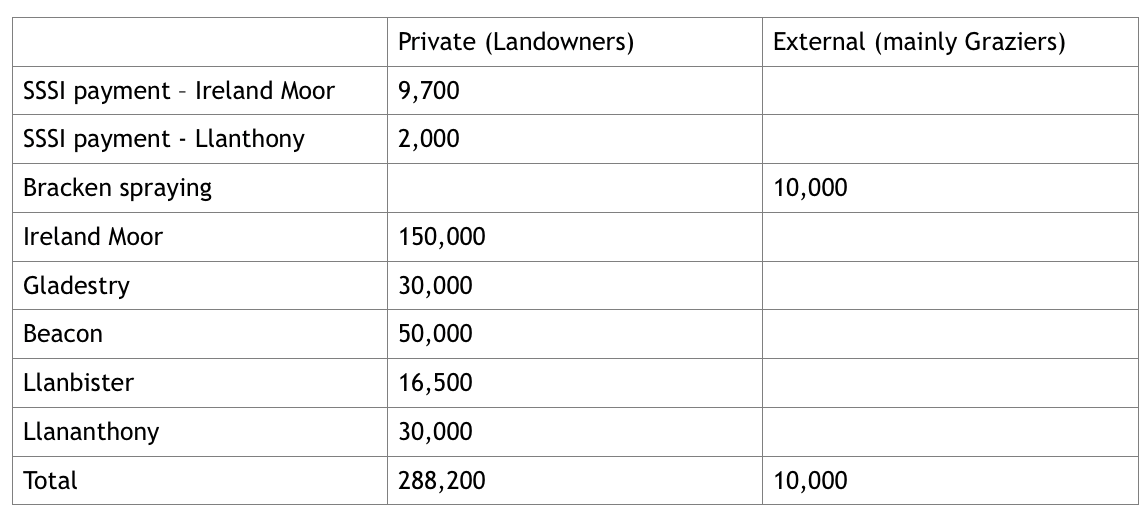

A payment of £9.7k/yr is made by NRW to support the management of the SSSI at Ireland Moor. This is connected to a habitat management agreement allowing heather burning, predator control and other actions to maintain and improve conditions for breeding birds (Grouse and waders).

This value represents a financial benefit to the estate. However, it is insufficient compared to the overall costs of managing the habitat, and not a reflection of the value society places on conserving wildlife.

Evidence on the monetary value to people of protecting wildlife in the UK is limited. One relevant study, by Christie and Rayment (2012), has values for improving the condition of SSSIs. The value for heathland is £556/ha/yr, and for bogs £1,021/ha/yr. The former value could potentially be applied to the SSSI area on Ireland Moor if the improvements in habitat are realised. However, this valuation captures the range of benefits sites provide to society (not only their wildlife value) and so would potentially double-count the other benefits analysed in this Section.

Ireland moor’s graziers also receive income from agri-environment schemes of around £150k p.a., which is paid to the collective of around 80 farmers on Ireland Moor, through Glastir Advanced. The primary aim of this payment and expense is to maintain the stocking densities that are able to support the health and biodiversity of the moorland habitat. These payments are designed on an income forgone basis, so is assumed to reflect level of expense incurred in complying with management requirements for the moor.

In addition to the above, Gladestry moor receives £30k per year from basic Glastir, and Ireland Moor is also in receipt of a capital grant for habitat management that is worth around £10k/year over 5 years. The other moors are assumed to receive funding of around £150k/year in total.

It is noted that the main Glastir payment agreement for the Moor ends in two years time. The account assumes it will be replaced with a similar payment arrangement, but this is subject to uncertainty. Agreements for these payments are typically 5 or 10 years in duration, the payments are taken to reflect the current contribution from society to maintaining the wildlife value of the moors. Therefore they are discounted over 25 years the same as other monetary benefits in the account. These figures are also recorded in the annual natural capital management costs.

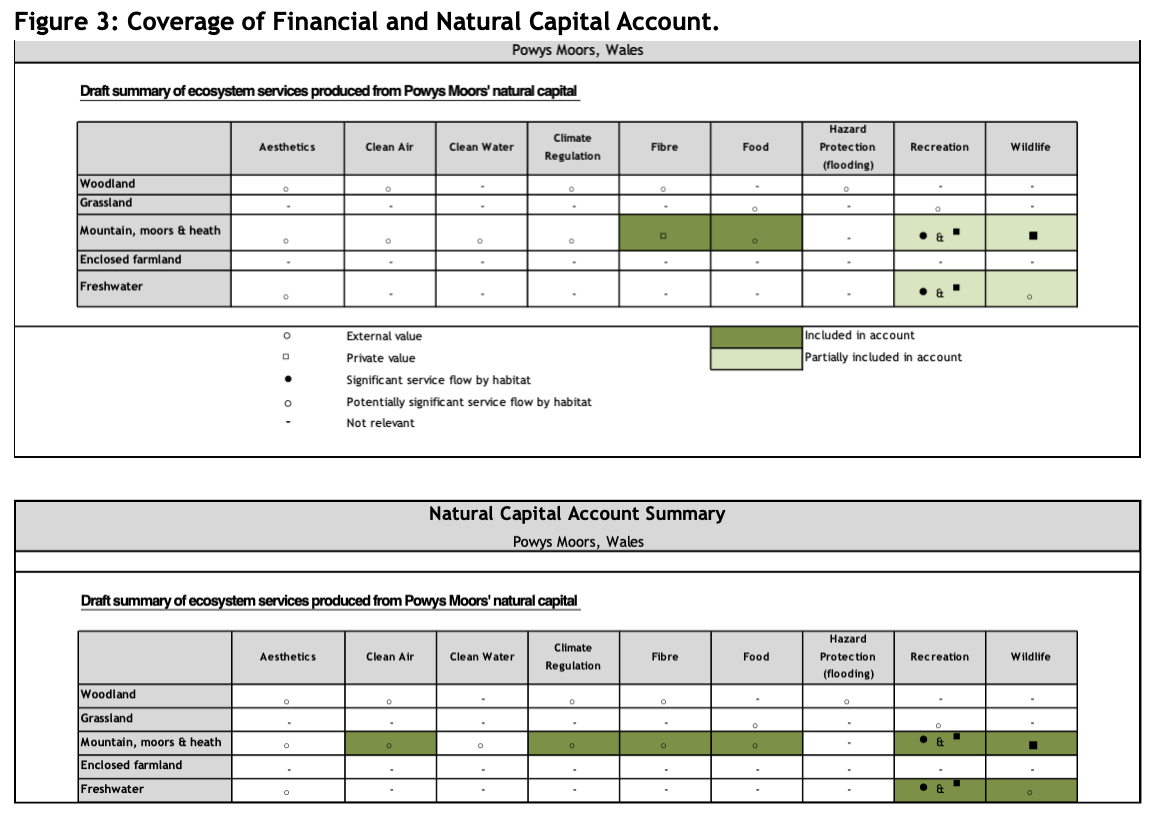

3.3 Account Coverage

The coverage of the natural capital account and the financial account for the estate are shown in Figure 3. This shows that the natural capital account captures more benefits, and some benefits more fully, than financial accounts. The private values in the account are shooting revenue (from wildlife) and the value of bracken cutting. Food production value is realised by farmers, rather than the land manager, so is an external value.

A number of rows and columns are retained in the matrices in Figure 3 to accommodate potential extensions of the account in future.

3.4 Natural Capital Maintenance Costs

The management costs for the Moors include the private costs of moorland management – estimated at £150k/yr for Gladestry and Ireland Moor and approximately £96k/yr in total for the other moors. They are also assumed to include the £150k/yr of Glastir advance payments to sheep farmers on Ireland Moor. There are also Glastir basic payments to farmers on Gladestry of £30k/year.

There is no distinction as to which management activities are to meet legal obligations, so in the account all expenditure has been assumed under ‘other maintenance provisions’. However, the designations as SSSI do bring certain requirements under law, so a portion of the management costs are likely to relate to legal obligations. Ireland Moor receives a capital grant of £10k/yr via Glastir Advanced, and a payment of £9.7k/yr from Natural Resources Wales (as described above under ‘biodiversity’), for managing the SSSI under a Section 15 management agreement.

The costs of managing the natural capital assets of the Powys Moors are approximately £416k/yr.

4. Conclusions & Recommendations

This Section provides interpretation of the natural capital account and suggests options for its future development and use.

Natural capital account conclusions

The Powys Moors are a distinct natural capital asset: they contain significant stores of carbon in peat soils; support extensive dry heath habitats with nature conservation and recreational interest; provide air quality and water regulating functions and contribute to a distinctive landscape. These benefits can be monitored through the physical data in the accounts natural capital asset register. Some of these benefits can be valued in monetary terms, and compared to the financial costs of managing the moors.

The majority of the assessed benefits relate to Ireland moor and Gladestry, which have more activities (e.g. shooting riding) but also better data.

The conclusions have a significant level of uncertainty, since valuation of several services has uncertainties. Physical measurements of recreational visits, and the amount of carbon sequestered (which is a complex area of science), have been estimated conservatively. Values for air quality regulation are highly uncertain as they are crudely interpolated from recent national modelling.

The account omits values for landscape, wildlife conservation, and regulation of the quantity and quality of water flows, and of flood hazard during extreme events. Therefore, there is an underestimation of benefits.

Future use of the account

Several of the key benefits assessed are subject to ongoing work which should provide better evidence for the account during 2018:

- The CEH modelling of UK air quality regulation by vegetation in the UK is being disaggregated to provide locally representative habitat values

In addition, further work is possible understand the value of the moors for water regulating services. However, these services require detailed local modelling to be quantified. This would be best be carried out in partnership with DCWW and NRW, as these benefits are best valued through the resulting avoided costs for those organisations.

Further work to improve understanding of the benefits and the accuracy of the account for the Powys Moors include, in approximate order of priority:

- Better understanding of soil chemistry and the storage, sequestration and emissions of green house gases.

- Applying better estimates of air quality regulation for rural areas (forthcoming in 2018).

REFERENCES

Aberystwyth University (2014) The farm Business Survey in Wales: Wales Farm Income Booklet Results 2013/14. Aberystwyth University, Institute of Biological, Environmental and Rural Sciences.

ADAS (2011) The Bedding Materials Directory. https://beefandlamb.ahdb.org.uk/…

BEIS (2017) Green Book supplementary guidance: valuation of energy use and greenhouse gas emissions for appraisal. https://www.gov.uk/…

Christie and Rayment (2012) An Economic Assessment of the Ecosystem Service Benefits Derived from the SSSI Biodiversity Conservation Policy in England and Wales, Ecosystem Services.

eftec (2015) Developing Corporate Natural Capital Accounts. For the Natural Capital Committee http://nebula.wsimg.com/…

Jones, H.E., Warkup, C.C., Williams, A.., Audsley E. (2008) The effect of genetic improvement on emissions from livestock systems. 59th Annual Meeting of the European Association of Animal Production, p 28. http://sciencesearch.defra.gov.uk/…

Jones, L., Vieno, M., Morton, D., Cryle, P., Holland, M., Carnell, E., Nemitz, E., Hall, J., Beck, R., Reis, S., Pritchard, N., Hayes, F., Mills, G., Koshy, A., Dickie, I. (2017). Developing Estimates for the Valuation of Air Pollution Removal in Ecosystem Accounts. Final report for Office of National Statistics, July 2017. https://www.ons.gov.uk/economy/environmentalaccounts/…

Natural Capital Coalition (2016) Natural Capital Protocol; Principles and Framework, Natural Capital Coalition, London. At: http://naturalcapitalcoalition.org/protocol/

Natural England (2012), Carbon Storage by Habitat: Review of the evidence of the impacts of management decisions and condition of carbon stores and sources, NERR043 at:

http://sciencesearch.defra.gov.uk/…

Natural England (2014) An Approach to Landscape Character Assessment, Natural England. https://www.gov.uk/government/…

NCC (2014) Towards a Framework for Defining and Measuring Changes in Natural Capital, Working Paper 1, Natural Capital Committee.

NCC (2016) How to do it: A Natural Capital Workbook. Defra. At:

https://www.gov.uk/government…

Sen, A., Harwood, A. R., Bateman, I. J., Munday, P., Crowe, A., Brander, L., Raychaudhuri, J., Lovett, A.A. Foden J. and Provins, A. (2014). Economic assessment of the recreational value of ecosystems: Methodological development and national and local application. Environmental and Resource Economics, 57(2), 233-249. https://ore.exeter.ac.uk/…

Smyth, M.A., Taylor, E.S., Birnie, R.V., Artz, R.R.E., Dickie, I., Evans, C., Gray, A., Moxey, A., Prior, S., Littlewood, N. and Bonaventura, M. (2015) Developing Peatland Carbon Metrics and Financial Modelling to Inform the Pilot Phase UK Peatland Code. Report to Defra for Project NR0165, Crichton Carbon Centre, Dumfries. http://sciencesearch.defra.gov.uk/…

UKNEA (2011) UK National Ecosystem Assessment. UNEP-WCMC. http://uknea.unep-wcmc.org/

University of Exeter (2016) ORVal – The Outdoor Recreational Valuation Tool. http://leep.exeter.ac.uk/orval/

This document has been prepared for Powys Moorland Partnership, by:

Economics for the Environment Consultancy Ltd (eftec)

4 City Road

London

EC1Y 2AA

Powys Moorland Partnership acknowledging the support of Rural Payments Wales, through the sustainable management scheme in funding the development of this account.

Study team:

Phil Cryle, Duncan Royle, Ian Dickie (eftec)

Reviewers:

Dr. Rob Tinch (eftec)

Disclaimer: This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law Economics for the Environment Consultancy Ltd, their members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.